Crocs Vs. Deckers: Gaining Footwear Market Share (NASDAQ:CROX) – Seeking Alpha

GordonsLife

Introduction

Crocs Inc (NASDAQ:CROX), and Deckers Outdoor Corporation (NYSE:DECK) compete in the global casual footwear market.

Crocs offers high quality, affordable, and personalizable clogs, sandals, and other products under the Crocs brand; it recently diversified its portfolio by acquiring HeyDude, a fast growing, value-oriented Italian casual shoe provider.

Deckers offers premium casual footwear, apparel, and accessories under the UGG brand; sandals, shoes, and boots under the Teva brand; relaxed casual shoes and sandals under the Sanuk brand, and athletic footwear for ultra-runners and athletes under the Hoka brand. In addition, it also offers value-oriented plush footwear under the Koolaburra brand.

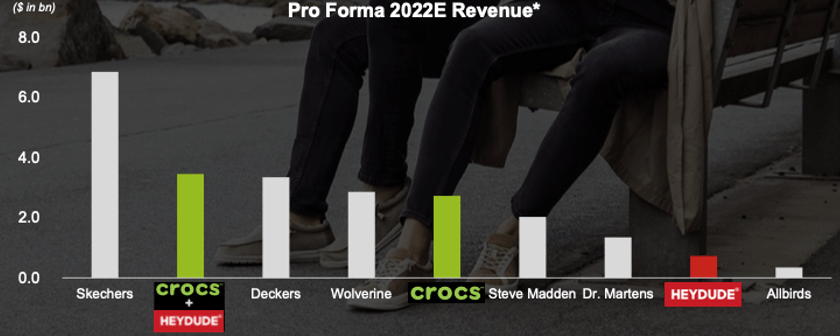

Crocs and Deckers are the second and third largest providers by revenue behind Skechers (SKX) (figure 1).

Figure 1: Revenue comparison of casual footwear providers

Crocs company presentation

Crocs and Deckers compete against Wolverine World Wide (WWW), which offers a wide range of formal, professional, recreation, athletic, and casual footwear under the Bates, Cat, Chaco, Harley-Davidson, Hush Puppies, Hytest, Keds, Merrell, Saucony, Sperry, Sweaty Betty, Wolverine, and Stride Rite brands; Sketchers, Steven Madden Ltd (SHOO), Allbirds (BIRD), Weyco Group (owner of Florseim (WEYS)), Ballys (owned by JAB Holding), Berkshire HH Shoe (a subsidiary of Berkshire Hathaway), and many others.

Crocs and Decker: Owners of iconic and practical footwear brands

As a self-professed non-shoe aficionado, most casual brands look and sound the same to me. However, Crocs and Deckers stand out as they both offer iconic, distinctive, and polarizing brands that evoke strong reactions amongst consumers. While detractors think they are ugly and fans adore and develop high emotional attachment to the products, it is hard to deny that they have powerful brands.

Deckers’ two key brands are Uggs and Hoka One One:

- Ugg boots was the generic name for a unique style of sheepskin boot that originated in Australia that was worn for warmth (while the origin of “ugg” is unclear, some have suggested that it is because the shoes are meant to be ugly). Deckers became the leading manufacturer of ugg boots and has actively against others, including Australian manufacturers who sell their “ugg” boots overseas.

- Hoka One One (pronounced Hu-ka onay-onay, a Māori term for “fly over the earth”): Acquired by Decker in 2013, it is lightweight shoe with a low weight to cushioning ratio and an oversized outsole to increase stability, but detractors have derided it as (figure 2). Initially embraced by ultra-marathoners but adopted by more mainstream runners; reduces runner’s risk of injury.

Figure 2: Hoka’s oversized sole

Deckers Outdoor

Over the years, Crocs has evolved from being the butt of internet meme jokes into with its own unique silhouette. As its proprietary Croslite material is versatile and cost effective to manufacture, the shoes are made into a wide variety of formats ranging from clogs, sandals, sneakers, boots, to platform shoes. Furthermore, as the material is lightweight, durable, easy to clean, comfortable after wearing for hours, it is put into a wide variety of uses ranging from leisure to hiking, and workers in healthcare, food service, and hospitality industries.

Today, Crocs counts major celebrities as spokespersons, including Post Malone, Justin Bieber, Drew Barrymore, and others, and attracts buyers who are young, expressive, self-confident, and active on social media. It has even moved into the luxury segment in partnership with Balenciaga, with its $850 high heeled crocs selling out within hours (figure 3). I cannot say that I understand the underlying consumer tastes driving these purchases but sales have taken off since the COVID-19 pandemic, and the Crocs Classic Clog was named in 2021.

Figure 3: Premium Balenciaga Crocs

DuckDuckGo images

Market segmentation

I segment the footwear market by price points and occasions. Apart from Hoka (which is a specialty running shoe), Crocs and Deckers products serve the value and premium segments for outdoor and casual users (figure 4).

Figure 4: Segmentation of the footwear market

|

Unbranded |

Value |

Premium |

Luxury |

|

|

Formal |

– |

Bruno Marc LifeStride |

Alden Florsheim (Weyco) Johnston & Murphy |

Alexander McQueen Ferragamo Gucci Jimmy Choos Prada |

|

Work |

– |

Crocs (healthcare, chef) |

Bates (WWW) Carolina (HH Shoe) HYTEST (WWW) Nursemates (HH Shoe) |

|

|

Athletic |

– |

Adidas ASICS Brooks Hoka (Decker) Nike |

Gucci Nike/Louis Vuitton Saint Laurent Rick Owens |

|

|

Outdoor / lifestyle |

– |

Sperry (WWW) Tevas (Decker) |

Dexter (HH Shoe) HH / Justin (HH Shoe) Harley Davidson (WWW) Merrell (WWW) Timberland |

|

|

Casual |

– |

Crocs (Crocs) HeyDude (Crocs) Keds (WWW) Koolaburra (Decker) Sanuk (Decker) |

Clarks Nike UGG (Decker) |

Gucci Versace |

Casual footwear industry trends and economics

(1) Long-term secular shift from the formal to practical, casual and comfort apparel and footwear:

Many white-collar offices have accepted semi-casual attire as the norm, and even some buttoned-down investment banks have allowed employees to dress-down on Fridays during the summer if they are not scheduled to meet with clients. (I note that many offices have relaxed the requirement that employees wear formal leather dress shoes, but some still discourage athletic or running shoes).

Healthcare, hospitality, and food service workers who work on their feet have similarly traded their nursing shoes and boots for shoes that are more comfortable and easy to clean (like Crocs). Similarly, people are increasingly opting for more comfortable footwear in their leisure and social activities.

(2) Away from uniformity to individualism:

Consumers are increasingly comfortable with footwear that express and convey who they are. This is a similar trend away as the consumer shift from plain Gold Toe socks (reminds me of Henry Ford’s “any color as long as it is black” policy) towards more colorful, whimsical, and offbeat socks. For example, manufacturers like Crocs enable customers to create customized footwear and Jibbitz—charms that snap onto customers’ Crocs shoes–enabling them to express who they are and what is important to them (figure 5). While I’d be the first to admit that this is not my thing, I note that consumers have been buying Jibbitz for over 15 years.

Figure 5: Customized Hello Kitty Crocs

DuckDuckGo images

(3) Fewer powerful, global brand in casual footwear compared to the athletic shoes segment:

They athletic and performance shoe segment is dominated by big and powerful brands like Nike (NKE), Adidas (OTCQX:ADDYY), Puma, many of which are endorsed by high profile athletes in all sports, some of whom even have their own brands (think Air Jordan or Kevin Durant).

In contrast, the casual footwear segment is far more fragmented and far fewer big brands. Even though some brands in the segment have reasonably high unaided brand recall (based on my non-scientific anecdotal poll), they do not have the same brand power.

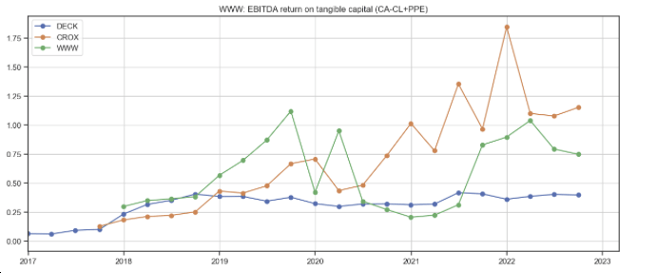

(4) High return on capital:

The footwear business is typically an asset-light business. Today, footwear companies concentrate on the high value parts of the value chain such as branding, design, and distribution, which deliver high returns on capital. Lower-value activities like manufacturing are typically outsourced to low-cost countries such as China, but has been migrating towards countries such as Vietnam, Sri Lanka, and other locations as rising labor costs, shipping congestion, and other concerns have caused companies to diversify their manufacturing bases.

The ROTC (return on tangible capital) on casual footwear is very high (figure 6), and is likely the reason why a super-investor like Warren Buffett has built and maintains a long-time presence in , which owns a portfolio of lesser-known shoe brands, ranging from the fashionable to medical, professional trade, law enforcement, and military footwear.

Figure 6: Return on tangible capital of casual footwear companies

Created by author using publicly available financial data

(5) Omnichannel selling, expanded digital presence:

Gone are the days when customers would walk into a store and walk out with the shoes they want or need. Even though footwear makers expect more of their sales to shift online, customers today typically search for, evaluate, purchase, and take possession of their shoes across both physical shops and online stores. As such, the ability to utilize online and social media for branding, leverage software to bridge the online and offline worlds (e.g., ), enhance the customer’s total experience, as well as to track and assist customers in their purchase journey are becoming necessary differentiators for footwear companies.

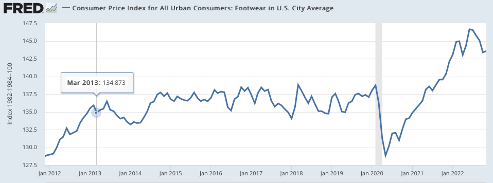

(6) Little price inflation:

There has been very little price inflation for footwear in the US over the last decade. Even as inflation heated up in 2022, the prices of footwear appreciated less than 3% as November 2022 (figure 7).

Figure 7: CPI for footwear in the US

St. Louis Fed FRED

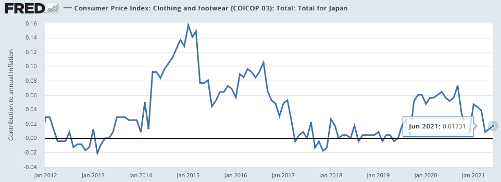

In Japan, price inflation for footwear has been similarly benign, remaining at around decade-ago levels as of June 2021 (the latest data available from the St. Louis Federal Reserve’s FRED).

Figure 8: CPI for footwear in Japan

St. Louis Fed FRED

(7) Winners take (almost) all:

As in most consumer segments, brand mindshare and distribution channels to reach end-customer matter, which along with growth and scale, create operating leverage and widen competitive moats.

Individual strengths

Crocs

Crocs is best known for its clogs and sandals that are made from its proprietary Croslite material. The reasons for the popularity of its products are the comfort with good support, ease of cleaning (which is important in some professions), and durability. Some people on social talked about owning and wearing their crocs clogs for a decade. As discussed in figure 5 above, Crocs clogs are also highly personalizable with the Jibbitz charms available from both Crocs and third-party providers on Etsy (ETSY) and other trading websites. Crocs footwear appears to have high net promoter score.

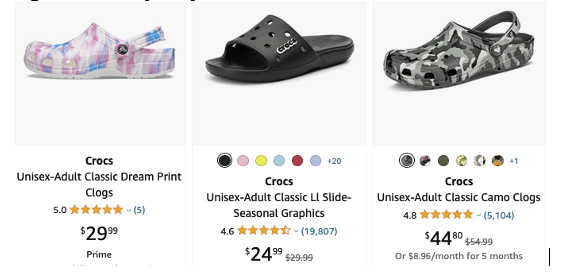

Crocs offers quality footwear at relatively low price points (~$20 and up) because the Croslite material is cheap to mold and the products are easy to assemble as they typically consist of very few parts (figure 9). As such, the gross margins are very high despite of the low-price points (see figures 13 and 19 below).

Figure 9: Crocs price points

Amazon.com

In 2021, the company acquired HeyDude, which also offers high quality casual shoes at low price points. HeyDude’s operating margins are still high but about 300bps below Crocs (as reported in the company’s Q3 2022 10-Q filing with the SEC), likely because they consist of more parts and may not be as cheap to produce or assemble as Croc’s Croslite-based products. However, I believe that as unit volumes increase as the product is put through Croc’s extensive distribution channels, Crocs will be able to negotiate more attractive prices with its manufacturers. Crocs management expects HeyDude’s long-term margins to be on-par with Croc’s at around 26% (see figure 22 below).

As emerging countries increase in affluence and their middle-class layer grows, the choice of footwear will likely shift from cheaper but flimsy flipflops currently popular in lower income areas to better quality, more stylish, and durable but still affordable sandals and clogs, and quality shoes (figure 10). As such, I expect emerging markets to be a longer-term growth driver for Crocs.

Figure 10: Crocs should benefit from the upgrade from flipflops to higher quality footwear

From low-cost flip-flops…

DuckDuckGo images

To sandals…

DuckDuckGo images

Then clogs…

DuckDuckGo images

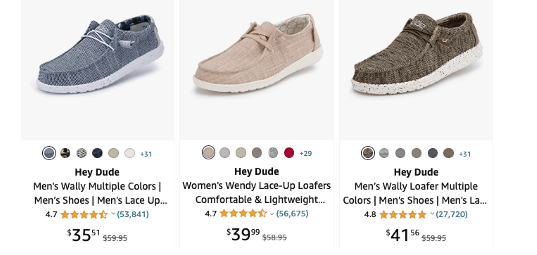

Followed by quality shoes like HeyDude, which have the same low-price point as Crocs clogs (beginning at $35-40), but can go higher for more fancy, intricate designs

Amazon.com

Deckers

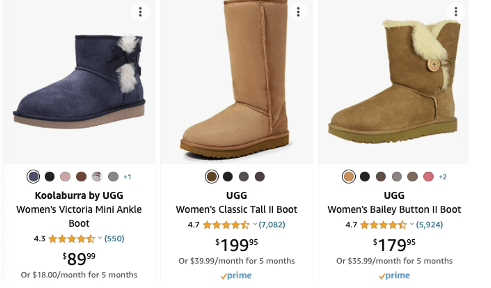

Deckers’ footwear typically have higher price points. Its UGG boots usually sell for well over $100, while its Koolaburra “value” extension go for about half of that (figure 11) but are still significantly more expensive than Crocs or HeyDudes. The products are well-loved by its core user base—they are made of sheep skin and lined with wool to keep feet warm and are typically worn in colder weather. The company has diversified the brand into summer footwear, but sales are still skewed towards the colder months (see figure 24 below).

Figure 11: UGG and Koolaburra price points

Amazon.com

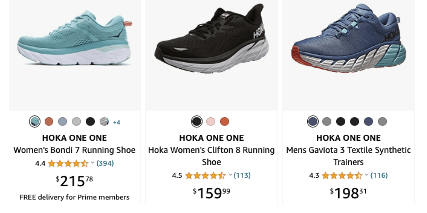

HOKA is specialty running shoe and Decker’s primary growth engine. It commands a higher price-point (figure 12) due to its lighter weight, superior cushioning, and stability afforded by its wider sole and attracts a specific but growing segment of serious runners. However, it faces tough competition from powerful global brands such as Nike, Asics, Brooks, New Balance, and Saucony, all of which, based on my price surveys on Amazon, have lower average selling price points than Hoka.

Figure 12: Hoka price points

Amazon.com

Decker also offers two additional brands, Teva and Sanuk, but both make up just a small (<5%) share of overall sales and are not growing quickly enough to move the needle. In fact, Sanuk sales have been declining over the last several years, for which see below.

Financial analysis and outlook

Crocs

Unit price:

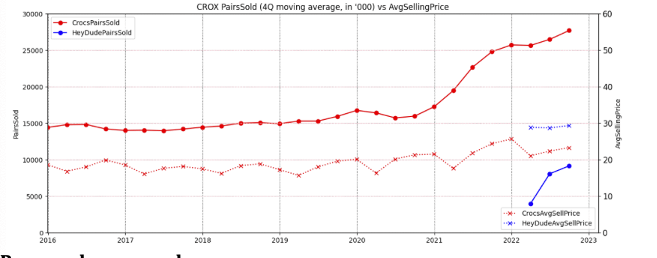

Footwear pricing has not been affected by inflation and generally been flat (see figures 7 and 8 above), and average selling price for both Crocs and HeyDude have not increased significantly (figure 13, dashed lines, right axis)

Pairs sold:

Crocs sold 103M pairs of footwear in 2021, up from 69M year ago (I used the Q4 moving average to smooth out seasonal fluctuations). The growth in 2022 for Crocs was strong; however, HeyDude has grown even more rapidly over the last year (red and blue solid lines, left axis), indicating that the shoes are moving well through the company’s distribution channels, has resonated with and gained acceptance amongst Croc’s own channels and distributions partners’ customer base. In Academy Sport’s Q2 2022 earnings call, CEO Steve Lawrence specifically called out Crocs and HeyDude in particular, noting that:

Other bright spots included … only big brands such as Crocs, Skechers, Adidas and Puma, which all ran increases for the quarter. We’re also excited to launch HEYDUDE in all stores in July to some time for back-to-school. We’re seeing strong early results and expect HEYDUDE to be a sales driver versus the remainder of the year.

Figure 13: Crocs average selling price and total pairs sold

Created by author using publicly available financial data

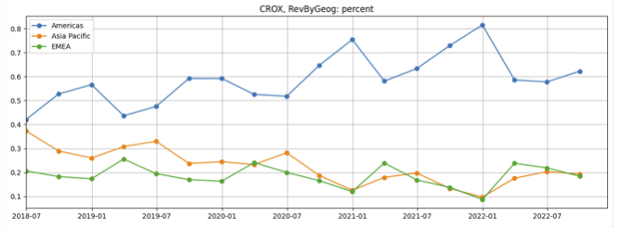

Revenue by geography:

Americas share of revenue increased from ~40% to ~60% while Asia Pacific has dropped in half from ~40% (close to the Americas) in 2018 to ~20%. EMEA has held flat (figure 14).

Figure 14: Crocs revenue percentage breakdown by region

Created by author using publicly available financial data

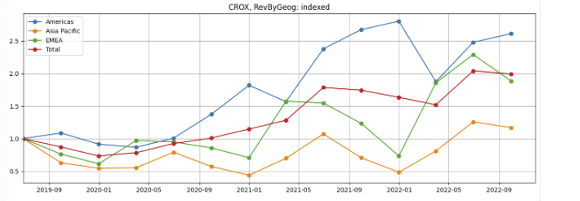

Compared to pre-COVID levels, revenue from the Americas were up 2.5x while Asia has hardly grown (figure 15, blue line vs orange line), likely due to the stricter lockdowns that has crimped consumer purchases.

Figure 15: Crocs growth by regions

Created by author using publicly available financial data

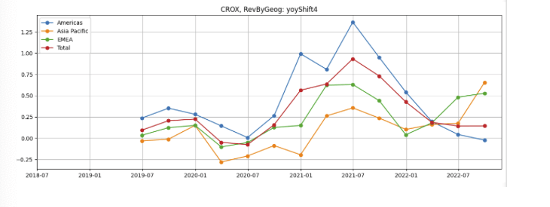

I believe the Asia recovery will be an important driver of growth over the coming years. China, the last holdout of any major economy, has finally , plans to on January 8, 2023, and expects to be fully open by Q3 2023. Unanticipated consequences from the surge in infections and risks of new coronavirus mutations aside, the Asian economic recovery and consumer purchases will accelerate Croc’s year-to-date growth from current levels (figure 16, orange line).

Figure 16: Croc year-over-year growth by regions

Created by author using publicly available financial data

In the company’s 2021 investor day, management noted that as China currently makes up less than 5% of total revenues, compared to 20% for some of its competitors, China sales have much room for growth. It expects its China share of total revenues to double to 10%, which sound reasonable to me, provided local manufacturers do not come up with imitations that snap up (no pun intended) Croc’s potential market opportunity. Management also expects more growth in India and Southeast Asia, and through its direct-to-consumer channels.

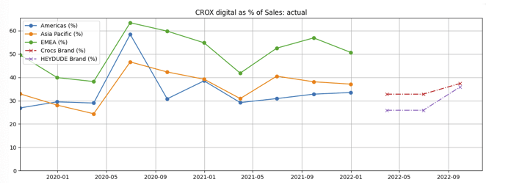

Digital sales from Croc’s own and distribution partners’ channels rose during the onset of the COVID-19 pandemic and currently make up about 37% (figure 17). Management expects to increase to 50%, or $2.5 billion, by 2026, but I view the growth in digital sales as a shift in the channels through which customers purchase the products rather than a driver of future demand.

Figure 17: Digital sales as % of total sales

Created by author using publicly available financial data

Non-clog products such as sandals and HeyDude shoes are also expected to benefit from Croc’s wide distribution channel, efficient supplier and logistics network, and marketing playbook.

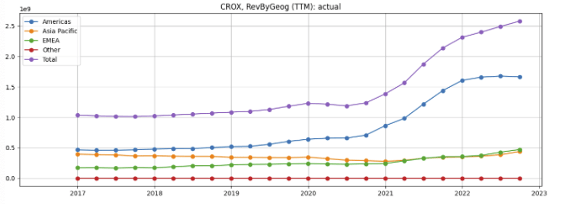

During the investor day in 2021, management has guided investors towards a 2026 revenue target of $5 billion (excluding HeyDude, which it had not yet acquired), roughly doubling from ~$2.5 billion in 2021. As the growth in the Americas appears to be leveling off after doubling in the last 5 years (figure 18, blue line), I suspect that management may be overly optimistic, and am underwriting to $3.75-$4 billion in revenue—this assumes that sales in the Americas grows by 50%, Europe continues on its growth trajectory, and Asia sales rebounds with the full re-opening of China, India and Southeast Asian countries.

Figure 18: Trailing twelve-month revenues by region

Created by author using publicly available financial data

Gross margins:

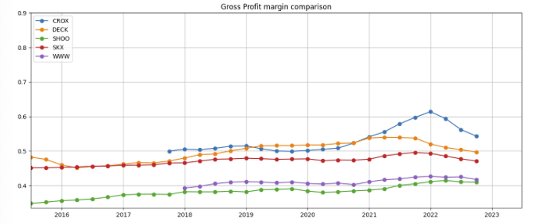

Gross margins rose steadily going into the COVID-19 pandemic but pulled back in 2022 (figure 19, blue line) as port congestion, high ocean freight rates, and supply chain problems which forced Crocs and its competitors to ship products by air, which drove the cost of revenue up.

Figure 19: Gross margins vs peers

Created by author using publicly available financial data

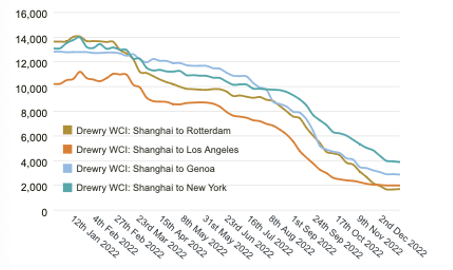

The headwinds due to port congestion appear to be subsiding—Shanghai to Los Angeles ocean freight costs have returned to $2,000 per container (figure 20), about one-fifth of year-ago levels. As such, gross margins are likely to bottom out and expand in the near future.

Figure 20: China to West Coast ocean container freight costs

Drewy

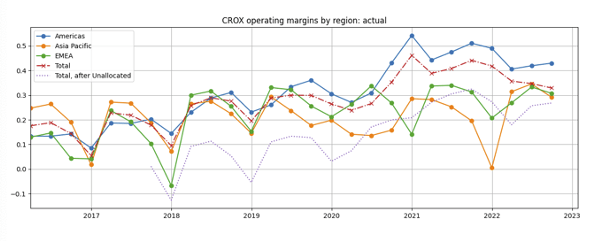

Operating margins:

I expect Crocs operating margins to rebound as a result of both higher gross margins as well as from the effects of operating leverage as revenues scale up (figure 21).

Figure 21: Crocs operating margin

Created by author using publicly available financial data

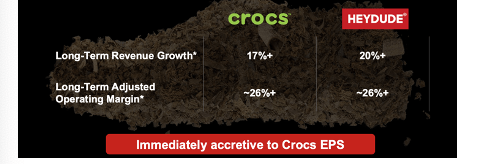

In the Q3 2022 10Q filing, the income from operations of HeyDude was 29.4%, compared to Croc’s 32.9% (figure 22). Interestingly, management noted in at the time of the HeyDude acquisition that Crocs and HeyDude both have similar adjusted long-term operating margins, suggesting that it does not expect long-term margin compression from the acquisition.

Figure 22: Crocs and HeyDude long term adjusted operating margins

Company presentation

Free cash flow

Management expects free cash flow to double to over $1b by 2026. If the company achieves this target, the current stock price (discussed below) would be a highly attractive entry point.

Shares outstanding

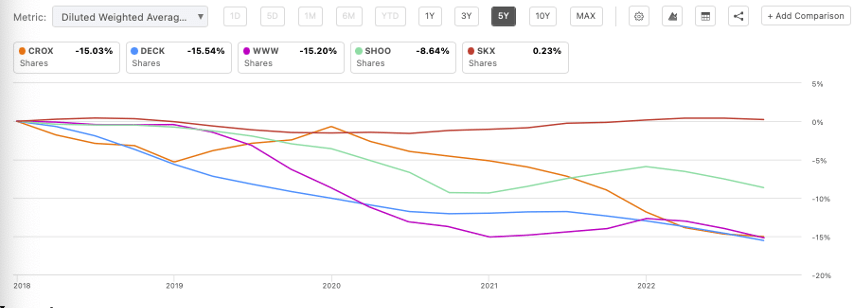

The strong cash flow generation has enabled Crocs, as well as competitors Decker and Wolverine, to reduce their fully diluted shares outstanding by 15% through share buybacks over the last 4 years (figure 23). Unfortunately, about $1 billion of Crocs shares were repurchased in 2021 when the stock was at its all-time highs. With the wisdom of hindsight, the company could have bought far more shares if it had spread out the repurchases into 2022. Crocs did not repurchase any shares in the first three quarters of 2022, likely because it does not want the balance sheet to be over-levered following the $2 billion spent on its acquisition of HeyDude, but as of September 30, 2022, management has authorization from the board to repurchase $1.05 billion more in shares.

Figure 23: Shares outstanding

SeekingAlpha.com charting

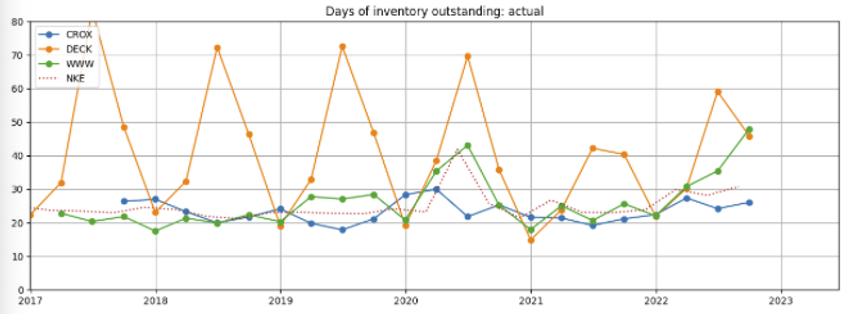

Inventory

Crocs inventory for Q3 2022 is on the higher end of its historical range (figures 24, blue line and figure 25) but not a cause for alarm.

Figure 24: Days of inventory outstanding

Created by author using publicly available financial data

Figure 25: Q3 days of inventory outstanding

Created by author using publicly available financial data

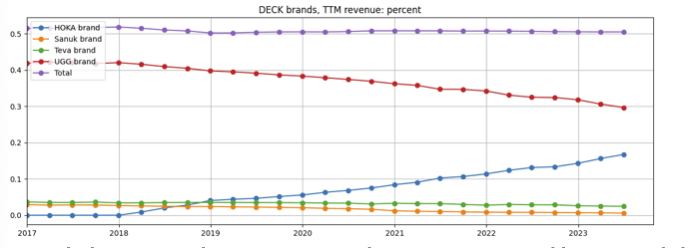

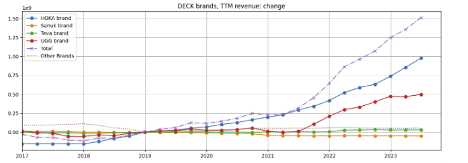

Deckers

I am focusing on UGG and Hoka as they are the two major sources of revenue (figure 26, red and blue lines). Teva and Sanuk each contribute less than 4% of revenue (green and orange) and are unlikely to move the needle.

Figure 26: Deckers percentage of revenue by segment

Created by author using publicly available financial data

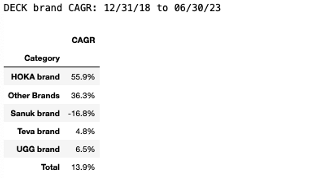

UGG is the biggest contributor to revenue and growing at a respectable compounded annual growth rate of 6.5% over the last 4 years (figure 27).

Figure 27: Deckers segment annualized growth rates

Created by author using publicly available financial data

However, Hoka has grown at a far higher annualized rate of 56% and contributed twice the revenue growth compared to UGG (figure 28, blue line vs red line). I believe Hoka’s growth is driven by the light weight, cushioning, and stability of shoes, which are attractive to long-distance runners. As running shoes need to be replaced regularly as the shock absorption cushion material deteriorates with repeated use, I believe Hoka’s revenue has some recurring characteristics. However, I do not have the ability to assess how much longer the brand can continue to grow at such rates before it plateaus off.

Figure 28: Deckers growth contribution by segment

Created by author using publicly available financial data

Financial metric comparison of Crocs vs Deckers

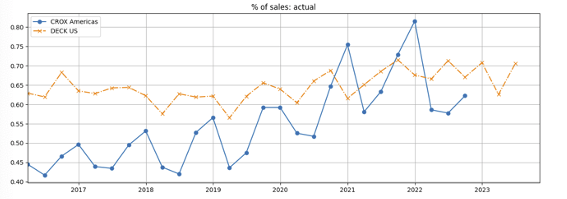

Geographical exposure:

US to international exposures are similar (figure 29), but it is likely that Croc’s international exposure will increase as the China market re-opens, driving its percentage of sales from Asia Pacific back to pre-pandemic proportions (see figure 14 above).

Figure 29: Comparison of sales in the US/Americas

Created by author using publicly available financial data

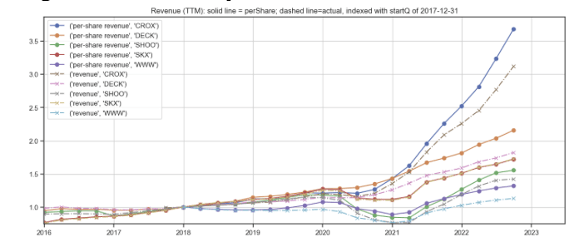

Growth:

Deckers revenue was up 80% over last 5 years (figure 30, pink dashed line) and 2.2x on a per-share basis (orange line) due to its share count reduction. In comparison, Crocs revenue was up over 3.2x over last 5 years (brown dashed line) and 3.7x on a per-share basis (blue line).

Figure 30: Revenue and per-share revenue comparison

Created by author using publicly available financial data

Gross margins:

Crocs has the highest gross margin, followed by Decker (see figure 19 above). Gross margins have contracted for both because higher container shipping costs and severe US port congestion has necessitated the use of more expensive air freight, but as discussed above, this squeeze appears to be moderating and container shipping rates are declining (see figure 20 above).

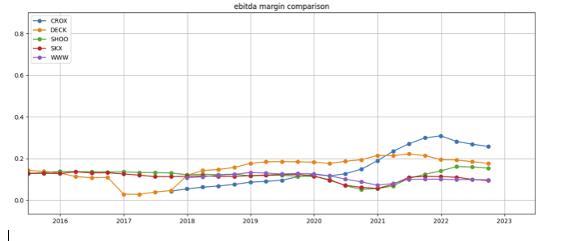

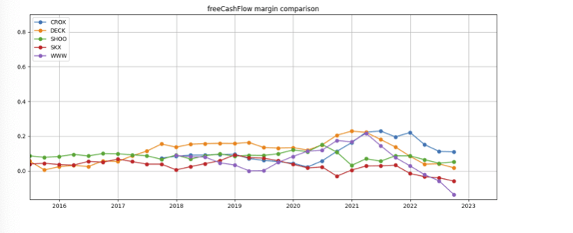

EBITDA and free cash flow margins:

Similarly, Crocs has higher EBITDA margins at around 30% compared to Decker’s ~20% (figure 31), as well as higher free cash flow margins (figure 32).

Figure 31: EBITDA margin comparison

Created by author using publicly available financial data

Figure 32: Free cash flow margin comparison

Created by author using publicly available financial data

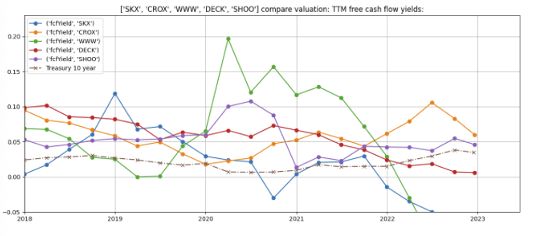

Valuation

Deckers has a higher valuation compared to Crocs (figure 33). Given Decker’s lower growth rate, I believe it is relatively fully valued.

Crocs management has expressed confidence in its continued long term growth—in its 2021 investor day, it put forth a target of a doubling of revenue by 2026 (excluding the acquisition of HeyDude)—this was followed by a revenue guidance cut (in Q2 2022) and several guidance hikes, including in the most recent Q3 2022 earnings report. Assuming management’s guidance is sound, the stock is cheap. Furthermore, I believe there is some margin of safety, even if earnings were to return to 2019 pre-pandemic levels. However, if some of my concerns discussed below hold true, the investment could turn out to be a nasty value trap.

Figure 33: Comparison of free cash flow yields

Created by author using publicly available financial and stock price data

Concerns

For both companies, my biggest concern is that even though both brands have been selling well for many years, footwear trends like Crocs clogs or UGGs could unexpectedly and abruptly go out of fashion like Beanie Babies. In mitigation, both brands have unique practical, comfort, and utilitarian characteristics I described above that go beyond fashion and should continue to attract new customers and keep existing ones returning for more.

Crocs

(1) Crocs could lose the under-penetrated Asian markets for clogs and sandals to enterprising local brands.

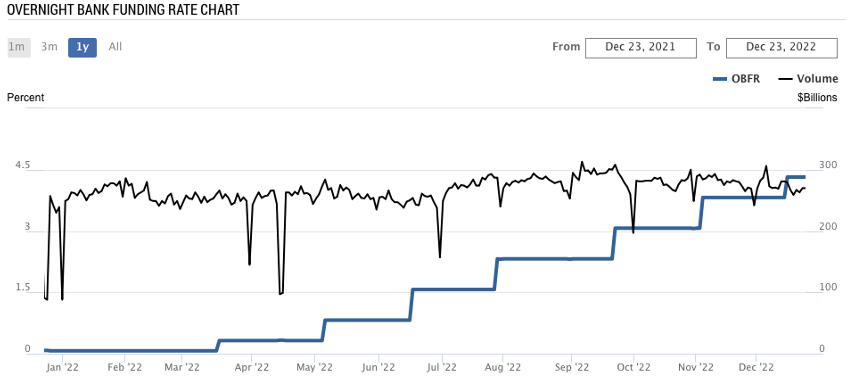

(2) The high debt load following the acquisition of HeyDude: Croc’s debt to EBITDA ratio stands at over 2.5x as of September 2022. In addition, the company’s ~$2 billion term loan facility (out of a ~$2.6 billion debt outstanding) has a variable interest rate based on the overnight financing rate published by the NY Federal Reserve Bank, which has risen by almost 300 bp in the last 10 months since the debt was issued (figure 34, blue line), translating into $60 million more in annualized annual interest payments.

Figure 34: Overnight bank funding rate by the NY Federal Reserve Bank

New York Federal Reserve Bank

Even though the company generates a healthy amount of cash flow, I believe it will take at least a couple more years before the company is a position to resume an aggressive share buyback program.

(3) The Croslite material which Crocs footwear are made from is non-biodegradable, which environmentally conscious millennials and Gen Z’ers may not appreciate. Crocs has begun working in partnership with Dow Chemical (DOW) to develop an alternative material using green materials.

(4) The investment community and SA writers seem very bullish—is this a negative contrarian sign?

Deckers

(1) HOKA competes in a field with very powerful global brand names such as Adidas, ASICs, Brooks, Nike, Puma, Saucony, and others. While it is currently targeting the long-distance running segment with lightweight, well-cushioned, and stable shoes, can it protect and continue expanding its market against competitors that have far larger marketing dollars and more extensive distribution?

(2) UGGs are oriented towards cold weather and sales are highly seasonal. Can they successfully diversify the brand into warm weather footwear?

In summary

Crocs and Deckers are leaders in the global casual footwear market, which have relatively few powerful competitors and generate very high returns on capital due to their asset-light model.

Both benefit from the long-term secular trends away from formal uniformity towards the practical, casual, and comfortable footwear through which consumers can express their individuality.

Since the onset of the COVID-19 outbreak, Crocs has delivered very strong growth and Deckers has maintained its steady growth trajectory. The growth is likely to continue with the rise of the global middle class, as Asian economies like China re-open, and consumers continue to opt for higher quality footwear.

Crocs is attractively priced but there are risks as described in the section on concerns above; in comparison, Deckers is fairly valued given its lower growth rate.

I rate Crocs a high-risk long-term accumulate and Deckers a hold.